Key takeaways

-

A physical shortage remains unlikely

-

Price risk for winter 2026/27 remains high

-

Storage levels and competition for LNG will be decisive

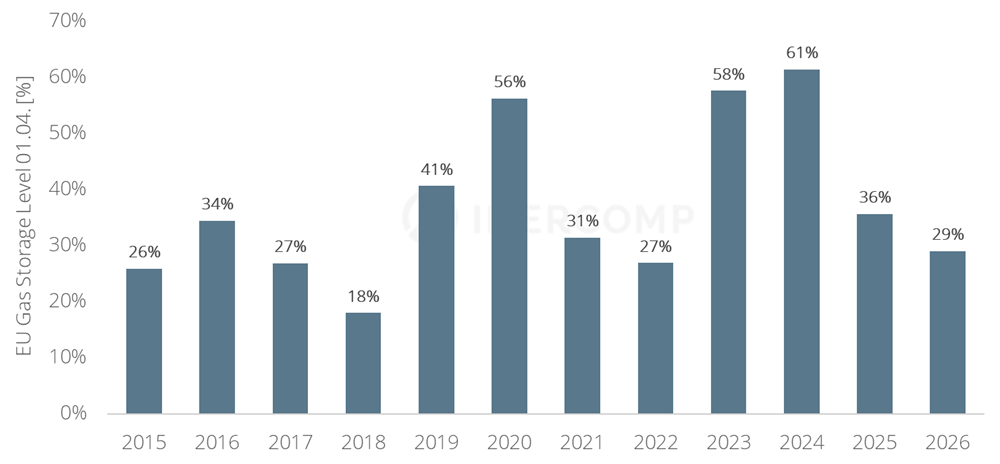

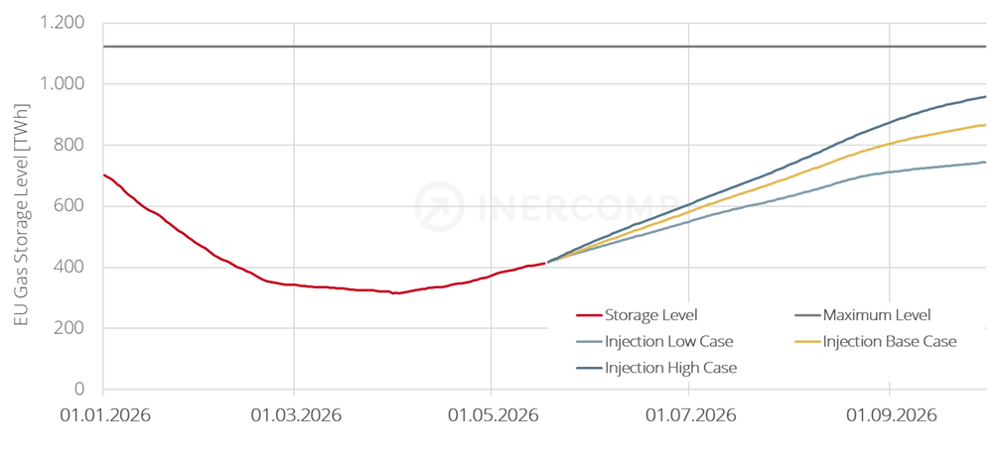

Europe entered the injection season on 1 April with storage levels of around 29%, the lowest level since 2022. At the same time, geopolitical tensions around the Strait of Hormuz are weighing on LNG availability, while Asian demand is picking up again.

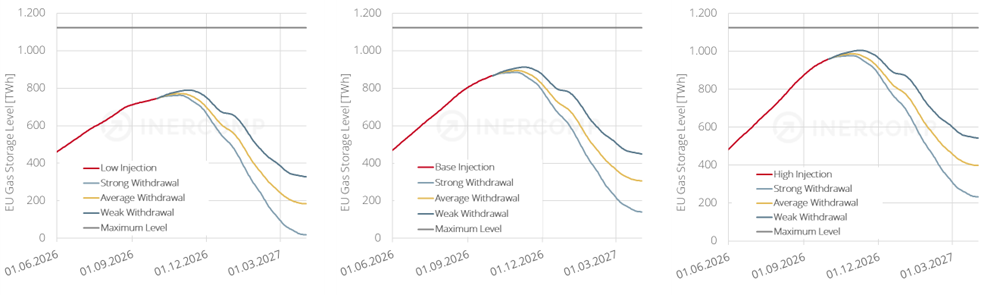

We modeled three scenarios to assess what this could mean for winter 2026/27 and why the central risk is price rather than physical supply.![]()